Newsletter

PNT Pulse — May 2026: LEO Stops Asking for Directions

The month LEO-PNT stopped being GPS's customer and started being its rival: ESA's Celeste sang from orbit, Xona banked a $170M Series C, and u-blox began wiring LEO signals into mass-market chips. A monthly read on where positioning, navigation & timing is actually heading.

PNT Pulse is my monthly read on where positioning, navigation & timing is actually heading — the signal beneath the press releases. Each issue does three things: gather the month’s most consequential GNSS, PNT and Earth-observation news, place each story against the wider market and its value chain, and draw out the “so what” you can actually use. The running order is fixed so you can skim — automotive & AI navigation first, then space (LEO-PNT) & defense PNT, then a rotating roundup of every other sector.

The 60-second version: This was the month low-Earth-orbit PNT stopped being a slide-deck idea. ESA’s Celeste demo satellites broadcast Europe’s first navigation signal from LEO, Xona closed a $170M Series C and put its first production-class satellite in orbit, and u-blox started wiring LEO signals into mass-market chips. Meanwhile driverless robotaxi fleets kept widening their service maps city by city — really a story about how much we now trust a fused position rather than a raw GNSS fix. One number to remember: GPS reaches the ground at about −127 dBm, below the noise floor. LEO-PNT shows up roughly 1,000× stronger. That asymmetry is the whole plot this month.

🚗 Automotive, AI & End-to-End Navigation

Driverless robotaxis kept widening their map — and quietly redefining GNSS’s job. Operators pushed paid driverless service into more metros this spring,1 and the technical story underneath is the same everywhere: the field is moving from modular “sense → perceive → plan → control” pipelines to large driving models that map raw sensor input straight to controls.2 Whether a fleet leans on lidar-plus-HD-maps or a camera-first stack, GNSS isn’t the answer in either — it’s one prior fused into a much bigger model. The “so what” for PNT: absolute position becomes a sanity-check and a geofence reference rather than the steering signal. Accuracy still matters, but integrity and robustness — does the receiver know when it’s being lied to — matter more.

Who else is moving. A quick lap of the field beyond the usual headline. Waymo remains the scale leader — past 2,500 vehicles and freshly capitalized with a ~$16B raise to push into a slate of new U.S. metros.18 Zoox (Amazon) is edging its purpose-built, steering-wheel-free pod toward paid rides in San Francisco in the back half of the year.1 Waabi is taking the freight lane: its generative-AI driver hit a Level-4 integration milestone on the Volvo VNL Autonomous, backed by a ~$1B round and an Uber robotaxi deal — while deliberately holding off on fully driverless launch until the platform is validated.19 And the China cohort is going global — Baidu Apollo Go, Pony.ai (targeting 3,000+ robotaxis this year) and WeRide are all racing into the Gulf, with services live or piloting across Dubai, Abu Dhabi and Saudi Arabia.20 The PNT thread tying them together: every one of these stacks uses GNSS as a fused prior, and as they spread into denser, more varied geographies, multi-constellation coverage and signal integrity matter more than another decimal of accuracy.

u-blox is bringing LEO-PNT down to the mass market. Following ESA’s Celeste launch (more below), u-blox said it’s assessing how LEO signals slot into multi-layer positioning, including early integration on its X20 GNSS platform, under an ESA NAVISP project.3 Translation: the chip vendors don’t see LEO-PNT as a niche defense play — they’re planning for it in cars and phones. And Murata signed an MOU with Xona to pair its RF/wireless know-how with Xona’s LEO positioning for industrial uses.4 Component-stage moves like these are the leading indicator that a technology is about to get cheap.

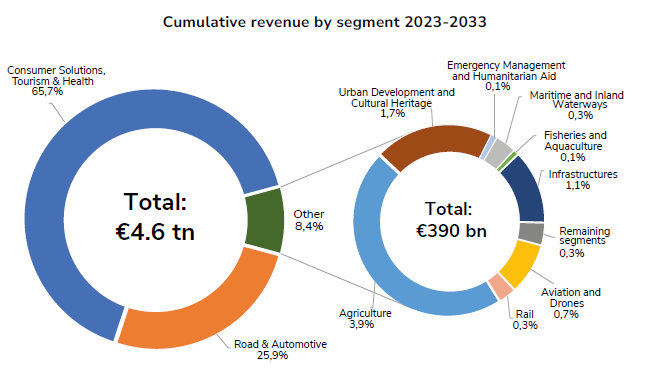

Anchor: Road & Automotive + Consumer Solutions together account for >90% of cumulative 2023–2033 GNSS revenue (EUSPA EO and GNSS Market Report, Issue 2, © EUSPA 2024). When chipmakers add a signal layer here, it’s aimed at the biggest part of the market.

Services — not hardware — are ~80% of GNSS revenue by 2033. Corrections and “trusted position” subscriptions are where LEO-PNT wants to sell. Source: EUSPA, 2024.

🛰️ Space (LEO-PNT) & Defense PNT

This is the section that earned the headline.

ESA’s Celeste broadcast Europe’s first navigation signal from LEO. The two demo satellites — IOD-1 (built by GMV) and IOD-2 (Thales Alenia Space) — launched March 28 on a Rocket Lab Electron, and by April 8 IOD-1 had transmitted the first dual-frequency L- and S-band navigation message ever sent from a European LEO satellite; IOD-2 followed on April 17.5,6 Celeste is explicitly framed as complementing Galileo and EGNOS — not replacing them — which is exactly the right framing.

Xona closed a $170M Series C and started launching. The oversubscribed round (led by Mohari, with Hexagon, Samsung Next, Craft, ICONIQ and others) funds satellite manufacturing toward a planned 258-satellite Pulsar constellation, and the company put its first production-class bird, Pulsar-0, up on SpaceX’s Transporter-14.7,8 On the government side, Xona is maturing its service for DoD via a $4.65M AFRL STAR-FISH award and a SpaceWERX follow-on9 — modest dollars, but the kind of pathfinder contract that precedes bigger ones.

Here’s the conceptual shift worth internalizing. For years LEO satellites were consumers of GNSS — comms birds that used GPS to know where they were. Now they’re becoming broadcasters of PNT. The geometry changes fast overhead, the signals land far stronger, and you get a fresh, independent layer that’s much harder to jam.

TrustPoint is filling the same lane from the defense side. It took a $4M SpaceWERX tactical-funding award for its independent PNT system10 and is collaborating with Hexagon NovAtel on C-band LEO-PNT — pairing a constellation builder with a receiver heavyweight.11 When NovAtel starts designing C-band into receivers, that’s a vote on where the puck is going.

And the reason all of this has urgency: jamming and spoofing keep getting worse. The FAA reports spoofing complaints more than doubled between January and June 2025, and observers recently spotted a new CRPA anti-jam antenna wired to BAE’s DIGAR system on USAF F-15Es during Operation Epic Fury.12,13 Anti-jam antennas treat the symptom one platform at a time; a stronger, multi-layer signal architecture treats the disease. That’s the bet LEO-PNT is making.

Anchor: EUSPA’s 2024 report framed LEO mostly as demand for GNSS. Eighteen months later the market has flipped toward broadcasting PNT from LEO. Assured-PNT is pegged around $846M (2025) → ~$10bn (2035) in third-party estimates — directional, not gospel, and the vendor forecasts vary widely.

🌍 Across the Rest of the Map

A quick tour of sectors that actually moved this month.

Maritime. EUSPA launched the EGNOS Safety-of-Life Assisted Service for Maritime Users (ESMAS) — an SBAS-grade accuracy and integrity-alert service for ships, extending EGNOS beyond its aviation home turf.14 Integrity (knowing when not to trust the fix) is finally treated as a service you can buy at sea, not just a nice-to-have.

Drones & U-space. Europe’s U-space framework keeps leaning on Galileo + EGNOS to enforce geofences around airports, events, and critical infrastructure.15 As drone density climbs, an authenticated, augmented fix becomes the thing that makes automated traffic management legally workable — not just technically possible.

Authentication, for everyone. Galileo’s OSNMA — free, cryptographic anti-spoofing built into the Open Service — moved from “initial service” to operational-adoption mode in 2026, with EUSPA running an OSNMA Day to push receiver makers along.16 This is Europe’s quiet superpower: the spoofing defense ships in the signal, for free, and it’s now Galileo’s job to get chips to actually use it.

Agriculture. Quieter month on the news wire — Deere’s precision-ag segment showed up mostly in financial filings rather than product launches17 — but it’s worth flagging that ag is ~46% of the “everything outside consumer and automotive” GNSS revenue slice, so I’ll keep a closer eye next month.

📈 Number of the month

~1,000×. That’s roughly how much stronger a LEO-PNT signal lands at the ground compared with a legacy MEO GNSS signal sitting below the noise floor. It’s the single physical fact behind every funding round and partnership above: stronger signal + faster-changing geometry = quicker fixes and a far steeper hill for a cheap jammer to climb.

🔭 What I’m watching next month

- Celeste, post-commissioning. First real positioning results from IOD-1/IOD-2 — does the in-orbit performance match the press release?

- Xona’s launch cadence. Pulsar-0 was the opener; the question is how fast production-class birds follow, and whether any automotive or critical-infrastructure pilots get named.

- OSNMA in silicon. Which mass-market receivers actually flip authentication on by default — that’s when anti-spoofing stops being a spec sheet line.

References

- Smart Cities Dive — robotaxi developments roundup

- arXiv — survey on end-to-end / large driving models

- GPS World — u-blox explores Celeste LEO-PNT for mass market

- GPS World — Murata & Xona sign LEO satnav MOU

- ESA — Celeste broadcasts first navigation signal from LEO

- Inside GNSS — GMV’s Celeste IOD-1 transmits first signal

- BusinessWire — Xona closes $170M Series C

- Electronics Weekly — Xona raises $170M for PNT network

- SpaceNews — USAF to explore Xona’s commercial GPS alternative

- Via Satellite — TrustPoint receives $4M SpaceWERX funding

- Inside GNSS — TrustPoint & Hexagon NovAtel C-band LEO-PNT

- The Aviationist — new anti-jam antenna on USAF F-15E

- RCR Wireless — rising GPS jamming threatens critical sectors

- EUSPA — new EGNOS Safety-of-Life service for maritime users

- EUSPA — Aviation and Drones (U-space)

- EUSPA — Galileo OSNMA Day 2026

- SEC — Deere & Co. 8-K (May 2026)

- Carbon Credits — Waymo hits 2,500 robotaxis in the US

- TechCrunch — Waabi raises $1B and expands into robotaxis with Uber

- Nasdaq — China’s AV push: Baidu, Pony.ai & WeRide lead the robotaxi race

Market fundamentals anchored to the EUSPA EO and GNSS Market Report, Issue 2, © EUSPA 2024. Third-party analyst forecasts are labelled as estimates and vary widely — read them as direction, not destiny. Sources are numbered in the References above.

Join the discussion

Thoughts, critiques, and curiosities are all welcome.