Newsletter

PNT Pulse — July 2026: The Rocket Company That Bought Its Own Satnav

A launch company agreed to buy the only commercial LEO-PNT service in orbit for about $8 billion, NIO synced a driver-assist update across two rival chip platforms, and GPS jamming kept scrambling ships in the Strait of Hormuz. A monthly read on where positioning, navigation & timing is actually heading.

PNT Pulse is my monthly read on where positioning, navigation & timing is actually heading — the signal beneath the press releases. Each issue does three things: gather the month’s most consequential GNSS, PNT and Earth-observation news, place each story against the wider market and its value chain, and draw out the “so what” you can actually use. Same running order every time so you can skim: automotive & AI navigation first, then space (LEO-PNT) & defense PNT, then a rotating roundup of every other sector.

The 60-second version: The headline is a company deciding it would rather own the whole PNT stack than buy pieces of it. A launch and satellite-manufacturing company agreed to acquire the operator of the only commercial LEO-PNT service flying today, in a deal worth roughly $8.0 billion — pad, satellite bus and PNT signal, all under one roof. Meanwhile, an automaker pulled off something quietly harder than it sounds: shipping the same driver-assist upgrade, on the same day, to cars running two completely different silicon platforms. And in the Strait of Hormuz, an average of ~972 ships a day kept getting shoved onto GPS maps that placed them in the desert or on dry land — a reminder of exactly why “own the whole stack” is suddenly a strategy and not just a slogan.

🚗 Automotive, AI & End-to-End Navigation

NIO shipped one driver-assist update to two rival chip platforms — on the same day. Its NIO World Model (NWM) upgrade rolled out in mid-June to more than 700,000 vehicles, and the notable part isn’t the size of the fleet — it’s that the same release landed simultaneously on cars running four Nvidia Orin-X chips and cars running NIO’s own in-house Shenji NX9031 silicon.1 That’s the first time an automaker has synced a driver-assist release across a general-purpose chip and a proprietary one. Under the hood, NIO describes a three-layer training setup — a world model, supervised fine-tuning, and closed-loop reinforcement learning — with the update newly able to read tidal lanes and variable overhead lane signs in real time.2 This is exactly the “large driving models” shift the field has been circling: perception and planning increasingly ride on one learned model rather than a stack of hand-coded rules, regardless of whose chip is underneath.

BYD, meanwhile, is pulling the chip in-house entirely. It unveiled the Xuanji A3, a 4nm automotive-grade driving chip it says natively supports L3 and L4 autonomy, and paired the announcement with a pledge of full damage coverage for both intelligent parking and its Urban NOA feature — effectively underwriting its own automation.3 When a system integrator starts designing silicon and backstopping the liability, that’s vertical integration eating two value-chain stages at once.

The “so what” for PNT: whether the brains underneath are Nvidia’s, NIO’s own, or BYD’s own, GNSS’s job in these stacks is unchanged and shrinking in the same specific way — it’s the absolute-position prior and geofence anchor that a much bigger perception model leans on, not the thing doing the driving. As more chip platforms enter the mix, the requirement that actually matters is that every one of them agrees on where “here” is, which is a robustness and integrity problem, not an accuracy one.

Who else is moving. Amazon’s Zoox unveiled a redesigned version of its steering-wheel-free pod in June, adding comfort touches ahead of large-scale production at its Bay Area plant — eventually 10,000 vehicles a year — while prepping to charge for rides and expand into new markets later this year.4 On the OEM side, Mercedes-Benz’s NVIDIA-built Alpamayo stack kept rolling out as a Level 2+ point-to-point system on the new CLA, a second concrete data point (after China’s NOA race) that “buy the reasoning stack from a chip vendor” is now a real OEM strategy, not just a NIO or BYD move.5 The PNT thread tying all of this together: every one of these programs treats GNSS as a fused prior, and as they multiply across chip vendors, OEM strategies, and geographies, multi-constellation reach and signal integrity matter more than another decimal point of accuracy.

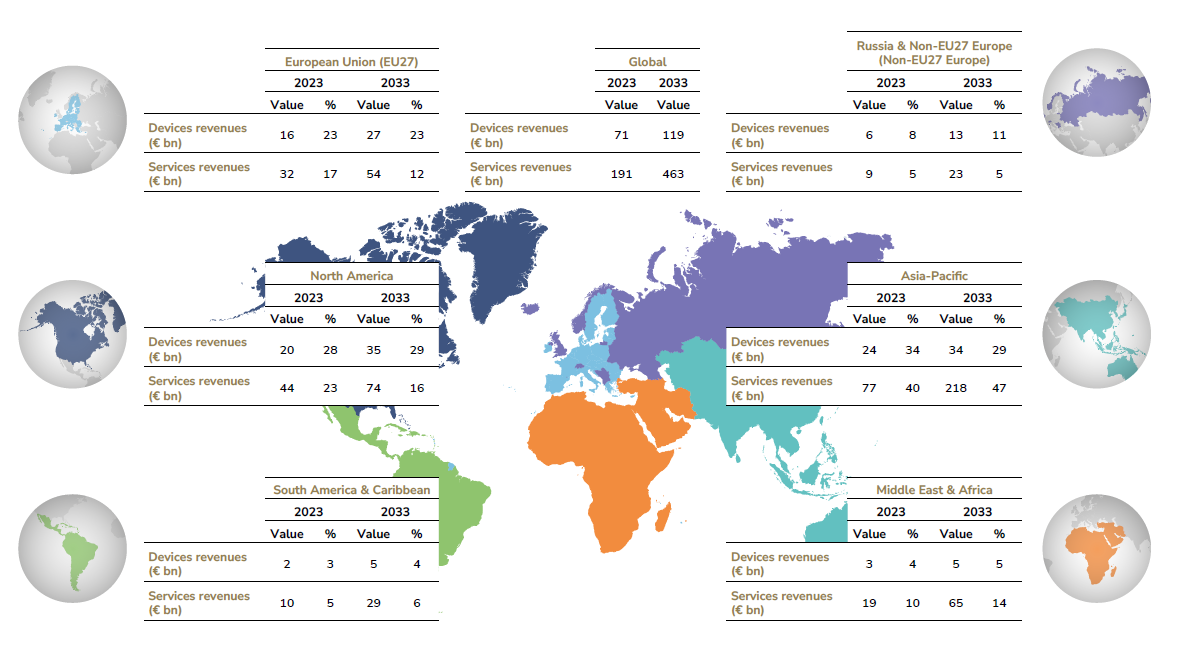

Anchor: GNSS device installed-base share in Road & Automotive is projected to grow from ~10% (2023) toward >15% by 2033 — the fastest-growing big segment as in-vehicle systems get fitted to new cars (EUSPA EO and GNSS Market Report, Issue 2, © EUSPA 2024). Every chip platform added to that installed base is another integrator that has to get positioning right.

NIO and BYD are both pushing further down this chain — from system integrator toward component designer. Source: EUSPA, 2024.

🛰️ Space (LEO-PNT) & Defense PNT

A rocket company agreed to buy its own PNT layer. Rocket Lab said it will acquire Iridium — the operator of the only commercial LEO-PNT service flying today, delivered via Iridium STL — in a cash-and-stock deal valuing Iridium at roughly $8.0 billion enterprise value ($54/share, split between $27 cash and stock).6 The deal is expected to close mid-2027, pending shareholder and regulatory approval, and it merges Rocket Lab’s launch vehicles (Electron, and the upcoming Neutron) and satellite manufacturing with Iridium’s operating constellation, spectrum, and PNT/direct-to-device business.7 Read that as the LEO-PNT story’s next chapter: last year’s news was about new players broadcasting PNT from orbit; this year’s is about consolidating launch, satellites, and the signal itself inside one company, so nobody else can hold your schedule hostage.

And the urgency for resilient PNT keeps compounding. GPS jamming and spoofing around the Strait of Hormuz averaged roughly 972 ships a day affected in mid-June, peaking at over 1,150 in a single day, with vessels’ AIS tracks erroneously placed in Iranian ports, the Omani desert, or near Dubai; transits through the Strait fell about 20% week-over-week as masters slowed down or rerouted.8 On the defense side, Pacific Defense won a U.S. Army contract to build a Block 2 Assured PNT plug-in card for the Army’s CMOSS Mounted Form Factor program — a ruggedized card that fuses GPS, alternative navigation signals, inertial sensors, and vehicle data to keep position and timing usable in contested, GPS-degraded environments.9 Modest as a line item, but it’s the hardware stage of “assured PNT” actually getting built, not just funded.

On the sovereign side, Europe kept its own PNT roadmap moving: Galileo’s Public Regulated Service is nearing formal declaration, second-generation Galileo satellites remain in full development with inter-satellite links and new atomic clocks, and EGNOS V3’s first critical design review is underway toward a 2027 target.10 None of it is as flashy as an $8 billion acquisition, but it’s the same underlying instinct — don’t leave your PNT layer to someone else’s roadmap.

Anchor: EUSPA’s 2024 report framed the Space segment mainly around GNSS receivers riding on satellites. Eighteen months on, the story isn’t just LEO satellites broadcasting PNT — it’s one company now owning the rocket, the satellite, and the signal. Third-party estimates still peg assured/resilient PNT around $846M (2025) → ~$10bn (2035); treat that spread as direction, not gospel.

🌍 Across the Rest of the Map

Rail leaned further on satellite positioning for safety-critical signalling. Europe’s rail sector continued rolling EGNOS-for-Rail into its R2DATO demonstrators, using satellite augmentation to help meet the integrity bar for Absolute Safe Train Positioning under ERTMS,11 while researchers presented a resilient train-positioning architecture pairing GNSS/IMU with the new 5G-based FRMCS radio standard, designed to keep working through GNSS-denied stretches of track.12 Rail has always needed integrity more than raw accuracy — a wrong position here doesn’t just annoy a driver, it can move a train onto the wrong section of track — so pairing GNSS with a redundant sensor set is the sector doing exactly what its risk profile demands.

Timing quietly became a boardroom risk. Data centers, telecom networks, and financial systems all lean on GNSS as their master clock, and as jamming and interference climb, “just trust the satellite” is looking thinner as a resilience plan — international timing standards now specify holdover clocks accurate to under 100 nanoseconds for weeks after a GNSS outage, precisely so critical infrastructure doesn’t go dark the moment a signal gets jammed.13 It’s an unglamorous story, but every AI data-center buildout and every 5G rollout adds another customer for resilient timing.

Insurance leaned harder on satellite-triggered payouts. The parametric insurance market — policies that pay out automatically once a satellite-measured threshold is crossed, no adjuster required — is estimated at roughly $22.6 billion for 2026, up from about $19.4 billion in 2025,14 and Mexico doubled the size of its own parametric catastrophe program to around $575 million for the 2026–27 season.15 EUSPA already flags Insurance & Finance as the EO segment forecast to lead by 2033 (~€900m); this is that forecast showing up as an actual government line item.

Demand for GNSS-and-EO-driven services keeps broadening past its traditional home turf — timing and parametric insurance are two of the less obvious beneficiaries. Source: EUSPA, 2024.

📈 Number of the month

$8.0 billion. That’s Rocket Lab’s proposed price tag for Iridium — and the single number that captures this month’s theme. From automakers syncing releases across in-house and third-party chips, to a rocket company buying its own PNT constellation, to defense buyers building assured-PNT hardware in-house: everyone with the balance sheet for it is choosing to own more of the stack, not rent it.

🔭 What I’m watching next month

- Regulatory road for Rocket Lab–Iridium. Whether the deal clears shareholder and antitrust review on schedule, and what Rocket Lab says about Iridium STL’s product roadmap once it’s not a standalone public company.

- Whether cross-chip-platform syncing spreads. NIO did it first; watch whether any Western or Chinese rival tries to match a same-day release across two silicon vendors.

- Hormuz jamming’s trend line. Whether the ~972-ships-a-day average eases as regional tensions cool, or becomes the new baseline maritime operators plan around.

References

- CnEVPost — Nio rolls out major driver-assist software update to over 700,000 users

- Electric Vehicles — Nio rolls out second-gen NWM update across three vehicle platforms

- CnEVPost — BYD unveils 4nm smart driving chip, Xuanji A3

- CNBC — Amazon’s Zoox unveils redesigned robotaxi ahead of upcoming expansion

- NVIDIA Blog — NVIDIA DRIVE AV software debuts in all-new Mercedes-Benz CLA

- PR Newswire — Rocket Lab to acquire Iridium in historic deal

- Marine Log — Rocket Lab in $8B Iridium acquisition

- Windward — GPS jamming disrupts ~972 ships a day in the Middle East Gulf

- Inside GNSS — Pacific Defense wins Army PM PNT contract for CMFF APNT Block 2 plug-in card

- ESA — Galileo Second Generation enters full development phase

- Europe’s Rail — Satellite positioning set to enhance train localisation

- Radiolabs — New train positioning with 5G-FRMCS and GNSS-IMU unveiled at ION Pacific 2026

- Syncworks — PTP and resilient timing in data centers

- New Space Economy — Satellite services for parametric insurance, market analysis 2026

- Artemis.bm — Mexico doubles parametric catastrophe insurance to ~$575m at 2026 renewal

Market fundamentals anchored to the EUSPA EO and GNSS Market Report, Issue 2, © EUSPA 2024. Third-party analyst forecasts are labelled as estimates and vary widely — read them as direction, not destiny. Sources are numbered in the References above.

Join the discussion

Thoughts, critiques, and curiosities are all welcome.